Find Foreclosures Today

Foreclosure is a legal process in which a lender takes ownership of a property when the borrower defaults on mortgage payments. If the borrower does not fulfill their payment obligations, the lender can reclaim and sell the property to cover the outstanding loan balance.

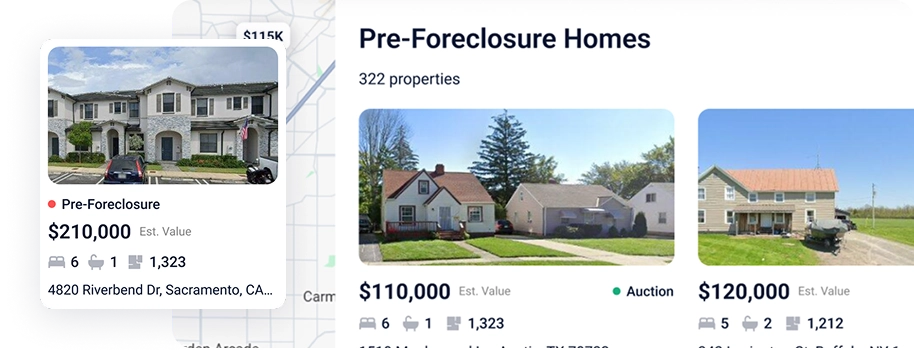

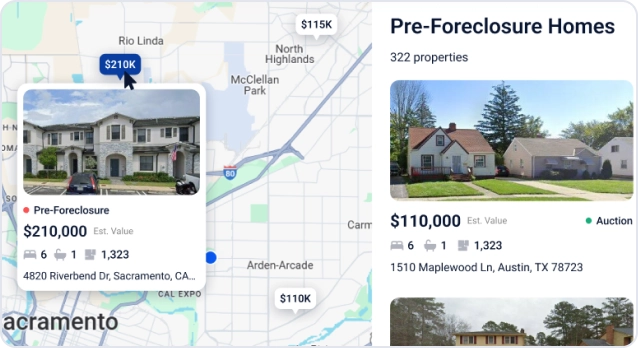

$210K

Daily-updated listings from multiple trusted source

Full access to pre-foreclosure, bank-owned, and auction properties

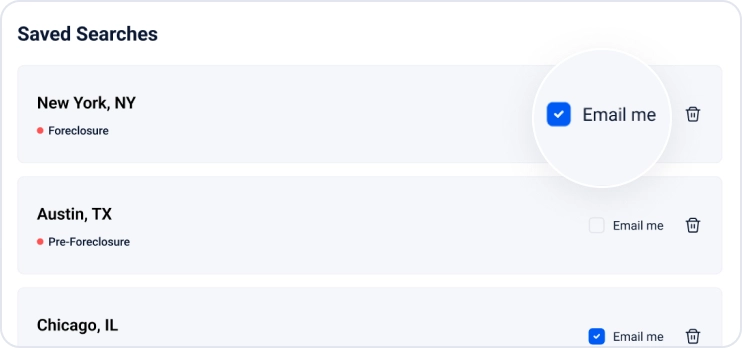

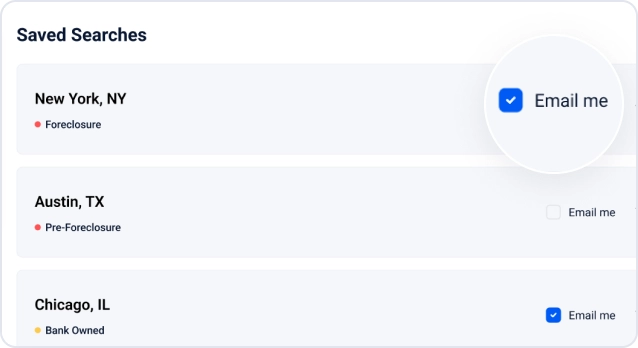

Customizable email alerts when new properties match your saved search

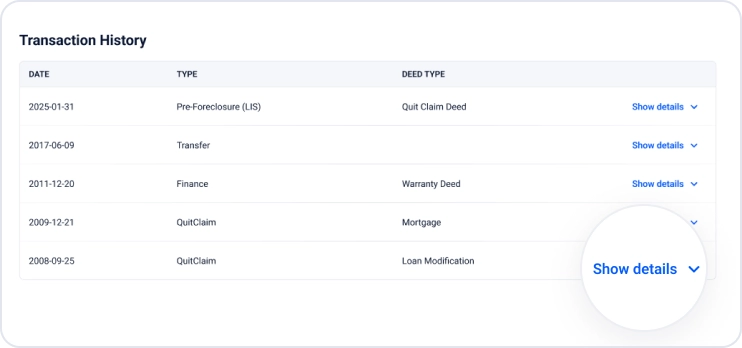

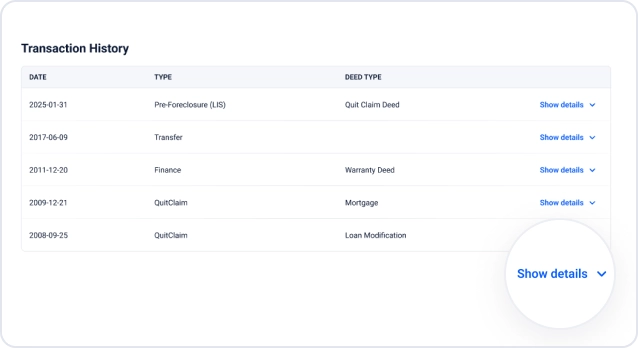

Detailed property data such as ownership records, property debt details, transaction history, sales history, tax records, and more

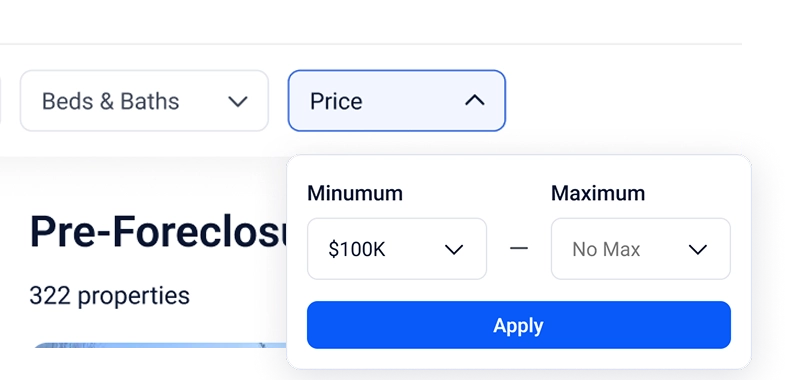

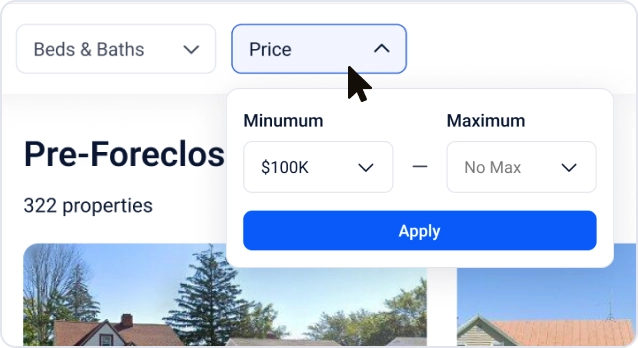

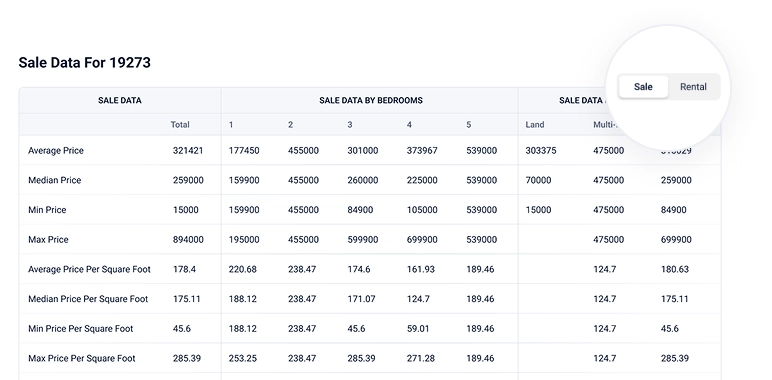

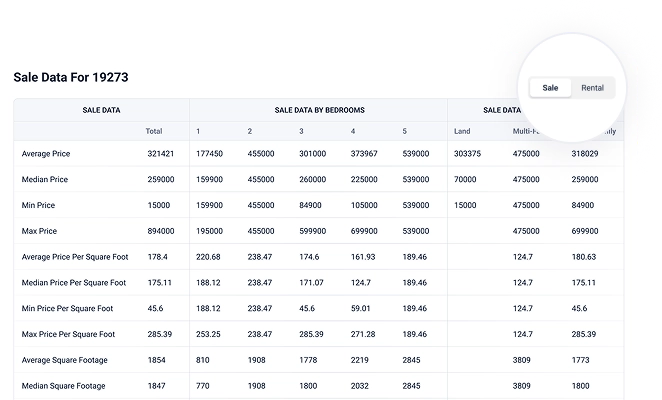

Market analytics featuring sale data by area, rental data by area, estimated monthly rent, comparable sales, property value estimate history, median property prices, and more

Explore homes on ForeclosureHub

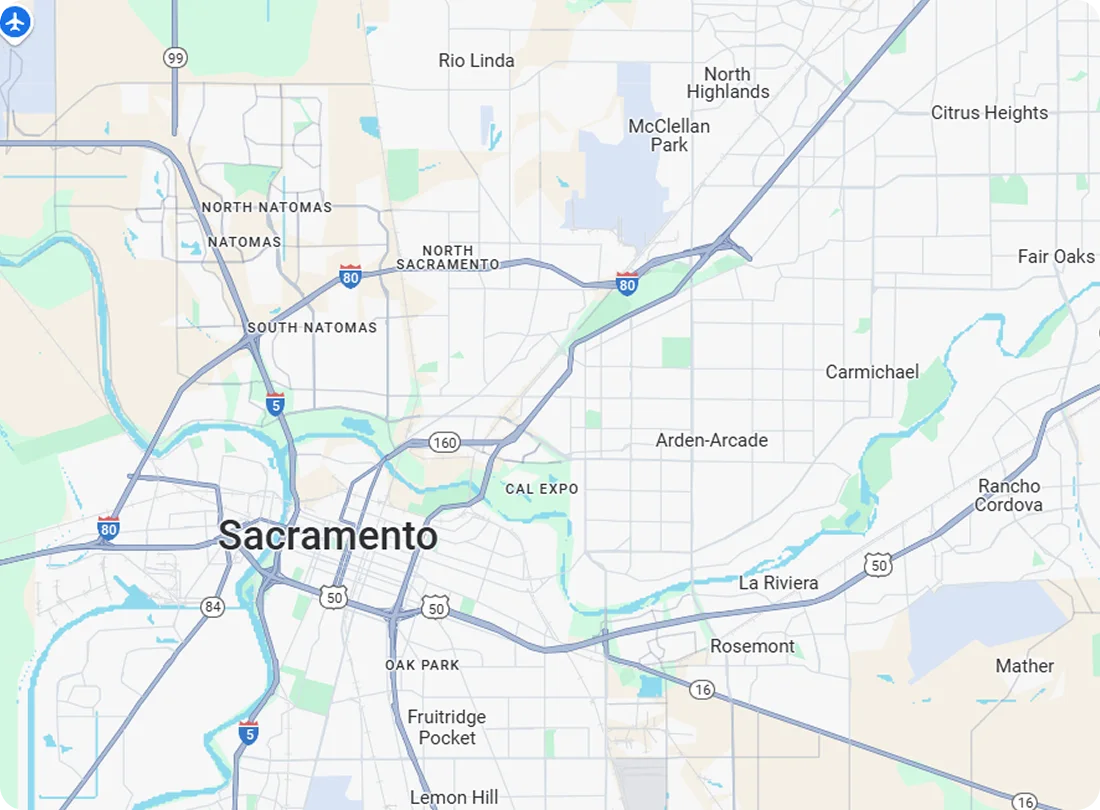

Search for foreclosures properties by state

- Alabama

- Alaska

- American Samoa

- Arizona

- Arkansas

- California

- Colorado

- Connecticut

- Delaware

- District of Columbia

- Federated States of Micronesia

- Florida

- Georgia

- Guam

- Hawaii

- Idaho

- Illinois

- Indiana

- Iowa

- Kansas

- Kentucky

- Louisiana

- Maine

- Marshall Islands

- Maryland

- Massachusetts

- Michigan

- Minnesota

- Mississippi

- Missouri

- Montana

- Nebraska

- Nevada

- New Hampshire

- New Jersey

- New Mexico

- New York

- North Carolina

- North Dakota

- Northern Mariana Islands

- Ohio

- Oklahoma

- Oregon

- Palau

- Pennsylvania

- Puerto Rico

- Rhode Island

- South Carolina

- South Dakota

- Tennessee

- Texas

- Utah

- Vermont

- Virgin Islands

- Virginia

- Washington

- West Virginia

- Wisconsin

- Wyoming